E-check, also known as ACH processing, is a form of electronic payment which transfers funds from one bank account to another quickly and securely. It is similar to writing a check in that the funds are taken from the sender’s bank account and deposited into the recipient’s bank account. The significant difference between e-checks and ACH payments is that an e-check is processed via the Automated Clearing House (ACH) Network. In contrast, regular checks are processed through a traditional banking system.

Although both processes involve electronically transferring funds, they have some distinct differences. First, when using an e-check, the sender must provide personal information such as their name and bank account number. This information is sent via a secure connection to be verified by their bank before the transaction occurs. On the other hand, with an ACH payment, no personal information needs to be sent over to verify the transaction.

Another critical difference between these two types of payments is how they are processed. An e-check requires authorization from both banks involved for it to process successfully. This authorization must come from a third party, such as the Federal Reserve or another intermediary service provider. With an ACH payment, there is no need for this type of authorization; it can be processed directly from one bank account to another without requiring any outside parties.

What is the difference between e-check and ACH?

E-checks and ACH are electronic methods of transferring funds. Still, ACH is a more widely used network for financial transactions, typically processed within 24-48 hours, while e-checks are the electronic versions of a traditional paper check, typically processed within 2-3 business days and less commonly used compared to ACH.

E-check vs. ACH:

E-check:

- The electronic version of a traditional paper check

- Funds are transferred directly from the payer’s checking account to the payee’s account

- Typically processed within 2-3 business days

- Less commonly used compared to ACH

ACH (Automated Clearing House):

- Electronic network for financial transactions

- Funds are transferred from the payer’s account to the payee’s account

- Typically processed within 24-48 hours

- More widely used and accepted compared to e-checks

- It can be used for recurring payments, direct deposit, and bill payments.

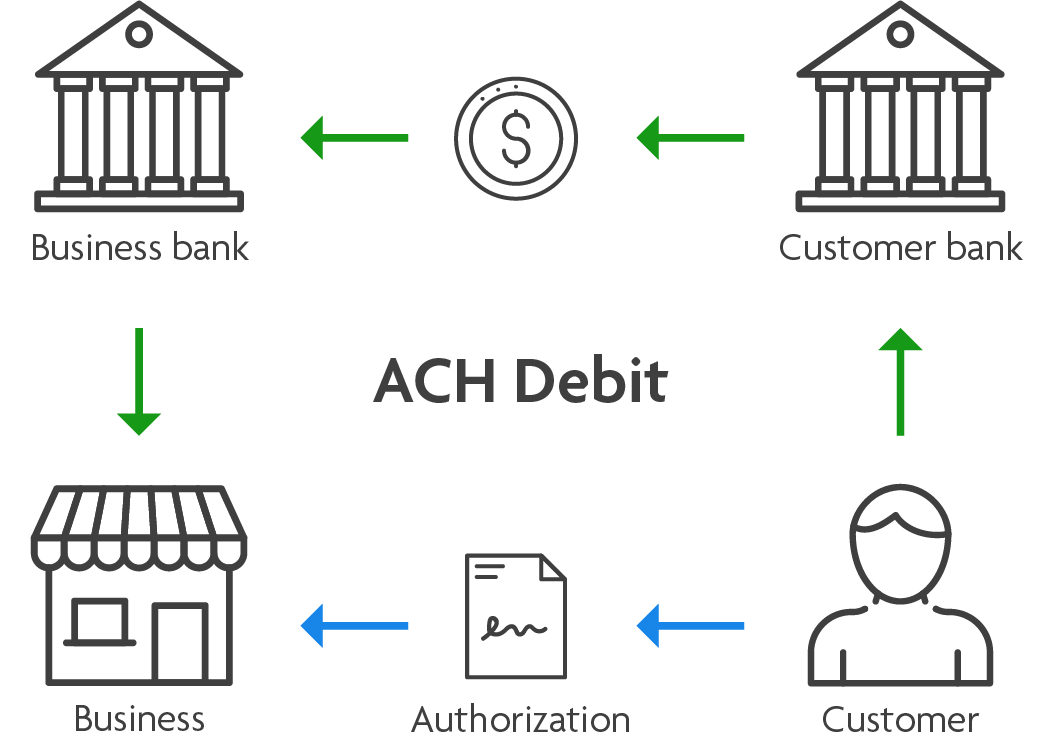

There is a significant distinction between electronic checks and electronic funds transfers (ACH). Specific organizations conduct ACH transactions by creating a recurring debit from a customer’s bank account using the banking information and an enrollment form. Payments are then processed on a monthly or quarterly basis. In addition, you can add a gratuity to your bill using ACH processing.

Finally, e-checks typically take longer to process than ACH payments do. Since it involves additional steps such as verification of personal information and authorization from both banks, it can take several days for an e-check transaction to complete—sometimes even up to five business days or more! An ACH payment usually only takes one business day or less to complete; however, due to its higher risk potential compared to other forms of electronic payment processing, some merchants may require a longer wait time before approving any payments coming through this network.

In summary, the main differences between e-checks and ACH payments are their processing times and required authorization levels—the former takes longer and requires additional steps than the latter. Both methods are secure forms of digital money transfer. Still, they have slightly different ways of verification, which can lead to differing completion times depending on what type of payment you prefer.

Newer technology is used, which wasn’t accessible when ACH processing started. The ACH network is used to handle payments for eCheck transfers. When you use an eCheck, you often make a one-time transfer between your bank accounts. It is faster than just a physical check, which takes longer. You’ll save money using checks instead of paper checks and credit or debit cards if you accept monthly recurring payments. Consider the positive aspects of the situation. In addition to saving money, eChecks are faster to process than traditional checks. The specific timeframes should be confirmed with the merchant services provider, though.

After leaving Wells Fargo Bank in 2014, Daniel began a career as a finance consultant, advising companies and individuals on economic policy, labor relations, and financial management.

At Promtfinance.com, Daniel writes about personal finance topics, value estimation, budgeting strategies, retirement planning, and portfolio diversification.

Read more on Daniel Smith's biography page.

Contact Daniel: daniel@promtfinance.com